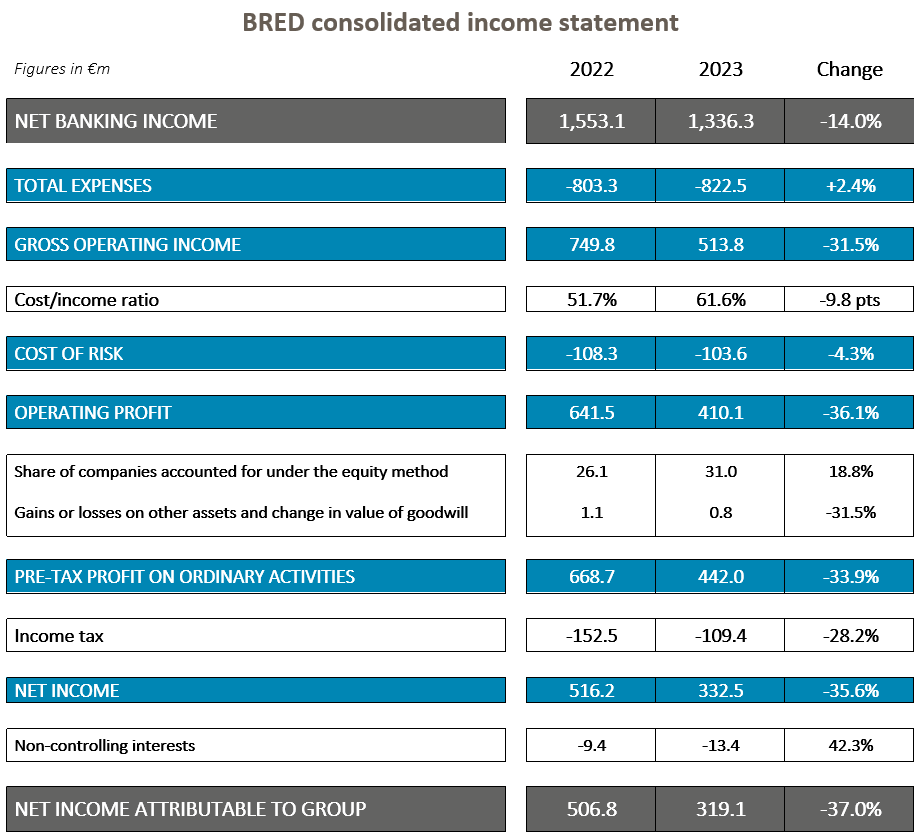

In a banking environment marked by rising interest rates, BRED made net banking income of €1,336m and net income of €319m. It continued to deploy resources to capture new sales markets while maintaining a very good level of solvency.

IN 2023:

- NET BANKING INCOME: €1,336M

- NET INCOME: €319M

- COST/INCOME RATIO: 61.6%

- EQUITY:€6.7bn

- CET1 RATIO: 16%

Jean-Paul Julia, Chief Executive Officer of BRED Banque Populaire, said: “2023 was a transitional year for BRED, with the rapid rise in rates impacting our financial results. Nonetheless, we continued drive sales momentum to serve our customers and members in all our regions. 2024 will see BRED adopt new ambitions, still with the aim of better supporting our customers and to develop business in our regions.”

BRED Banque Populaire generated net banking income (NBI) of €1,336m, down 14% compared with 2022.

This decline can be attributed to the specific environment in 2023, during which interest rates rose rapidly and penalised all our business lines, with the exception of the international activities, which saw further steady growth.

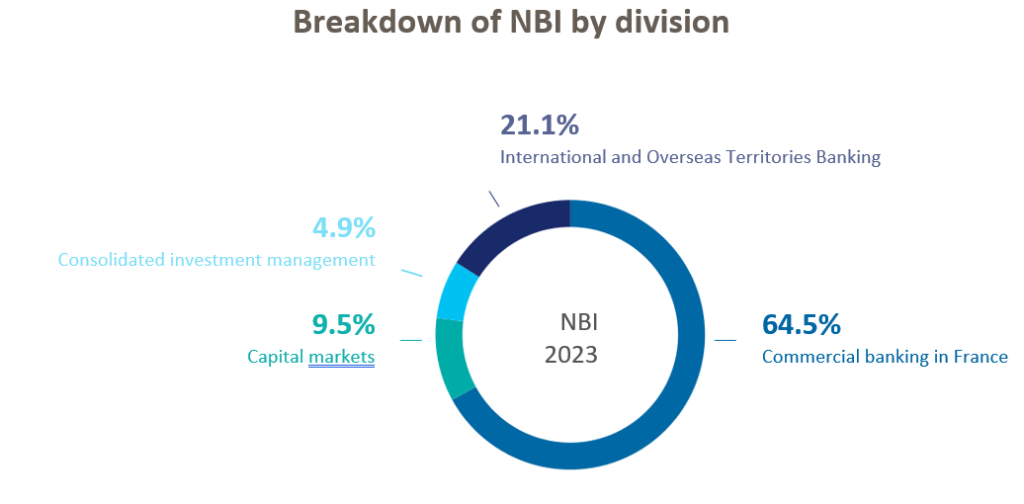

Commercial Banking France

Commercial Banking in France (including ALM) registered a 14.8% fall in NBI. It was impacted by the rise in the cost of resources and in the cost of refinancing, while net interest margin fell by 34%. This fall was partially offset by an increase in commission income (+8%), in line with the strong growth in our customer base across all our customer segments.

International and overseas territories banking

The International and Overseas Territories Banking division reported an 18.9% increase in NBI at constant currency. It benefited from excellent results in commercial banking in the Pacific and the Horn of Africa, and strong trade finance activity at BIC BRED Suisse (+15%).

Capital markets

The trading floor saw a decline in its results (-23%) in 2023 compared with 2022. It achieved considerable growth in sales activity, leading to a sharp increase in volumes processed. For the first time, BRED was recognised as the leading bank in Europe in the placement of short-term debt for domestic and international issuers.

Consolidated investment management

After a high-level in 2022, consolidated investment management fell sharply in 2023 (-40.8%), reflecting economic uncertainties linked to the rise in interest rates.

Operating expenses

Total operating expenses remained under control, increasing by a total of 2.4%,reflecting ongoing investment in information systems and operational efficiency, as well as the recruitment and training of employees. Strong development of subsidiaries in France and outside of France also contributed to the increase in the Group’s operating expenses.

Cost/income ratio

The cost/income ratio came to 61.6%, remaining at a very good level.

Cost of risk

The total cost of risk was €103.6m, down 4.3% despite a slight increase in the cost of risk on impaired loans (+3.4%). The cost of risk relative to outstanding loans remained under control.

BRED Group share of net income

BRED Group’s share of net income reached €319m, its third largest level over the past ten years.

Very solid solvency and liquidity ratios

Shareholder’s equity stood at €6.7bn, up 8.3% over the year.

The CET1 solvency ratio was a very good 16%.

The LCR liquidity ratio stood at 131% at 31 December 2023, the regulatory minimum requirement being 100%. BRED’s NSFR (net stable funding ratio) was 110% at 31 December 2023, the regulatory minimum requirement being 100%.